Reservar cita

Third Party Administrator Health Insurance: A Guide to Cross-Border Claims

Por

Por

In third party administrator health insurance, a third party administrator (TPA) runs the plan mechanics for a self-funded employer. It adjudicates claims, pays providers, and handles eligibility and reporting, while the employer carries the financial risk. Most of the U.S. group health market now works this way. When a member is treated abroad, the episode still has to reach the TPA as a clean, adjudicable claim. This guide covers what a TPA does, where cross-border care fits its workflow, and the documentation that makes a foreign claim pay without friction.

What is a third party administrator?

A third party administrator (TPA) is a licensed company that runs a health plan on the employer’s behalf and does not carry the insurance risk. It handles claims adjudication, provider payments, member services, eligibility, and reporting (National Association of Insurance Commissioners (NAIC), Third-Party Administrators). The employer funds the claims and owns the risk. The TPA prices, processes, and pays claims against the plan’s rules and reports back to the plan sponsor. Some plans buy this as administrative-services-only (ASO) support from a carrier; others use an independent TPA.

Third party administrators in insurance sit between the plan and its providers, which is why they matter to a self-funded employer. The model now covers most of the group market. In 2024, 63% of covered workers were in self-funded plans: 79% at large firms and 20% at small ones (KFF, 2024 Employer Health Benefits Survey). Every one of those plans depends on a TPA to turn care into a paid, documented claim.

How does cross-border care fit third party administrator health insurance?

Cross-border care enters a TPA’s workflow in one of two ways: a self-funded plan adds a medical-travel benefit, or it approves a single complex case abroad as a one-off. Either way the requirement is the same. The foreign episode has to arrive as a clean, adjudicable claim: itemized, coded where possible, and tied to an authorization.

The difficulty is administrative, not clinical. A foreign claim tends to stall on a short list of predictable friction points:

- Language: clinical records and invoices in Spanish or Portuguese that adjudication staff cannot read.

- Non-US coding: procedures billed under a different coding standard, or not coded at all, so the claim will not map to the plan’s rules.

- Currency: charges in local currency with no fixed conversion or reconciliation to the plan’s allowed amount.

- Proof of delivery: no clean evidence that the care authorized is the care that was actually delivered.

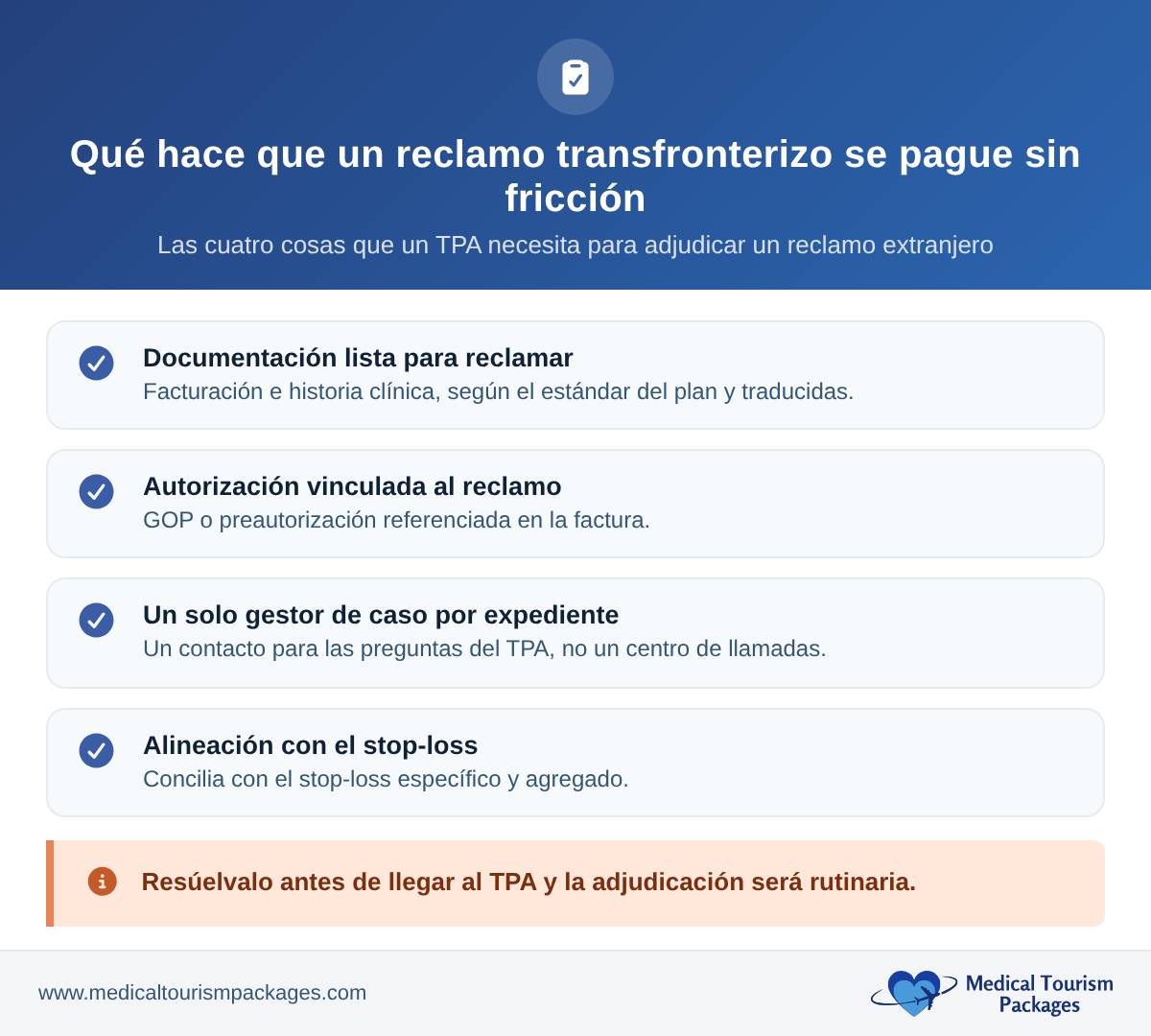

Resolve these before the claim reaches the TPA and adjudication is routine. Leave them for the adjudicator to chase and a legitimate case can sit in pending for weeks.

How does a cross-border claim move from authorization to adjudication?

A cross-border claim follows the same path every time, and each step feeds the next:

1. Authorization and GOP. The plan pre-authorizes the case and a Guarantee of Payment (GOP) is issued to the treating facility, fixing the scope and the price before travel.

2. Care delivered abroad. The member is treated at the accredited provider, and the coordinator tracks the case against the authorization so the delivered care matches what was approved.

3. Documentation assembled and translated. Itemized billing, clinical records, and proof of delivery are compiled to the plan’s standard and translated into English.

4. Claim submitted to the TPA. The claim reaches the TPA already itemized, coded where possible, and referenced to the GOP: one clean file rather than a stack of foreign paperwork.

5. Adjudication and payment. The TPA adjudicates against the plan’s rules and pays the provider, or reimburses per the benefit design.

6. Stop-loss reconciliation. If the case is large enough, the same documentation supports the specific or aggregate stop-loss filing without a second collection effort.

The point of doing this in sequence is that nothing has to be reconstructed after the fact. Each artifact the TPA needs is captured while the case is live, not chased down once the member is home.

What makes a cross-border claim pay cleanly?

Four things turn a foreign episode into a claim a TPA can adjudicate without back-and-forth. This is the layer a coordination partner supplies:

- Claims-ready documentation: itemized billing, clinical records, and proof of delivery, organized to the plan’s standard and translated into English alongside the original.

- Authorization tied to the claim: a Guarantee of Payment (GOP) or pre-authorization referenced directly on the invoice, so the adjudicator can match the bill to the approval instead of opening an investigation.

- A single case manager per file: one named contact who can answer the TPA’s questions on the specific case, rather than a call center with no line of sight into it.

- Stop-loss alignment: documentation built so the case reconciles against both the plan’s specific (individual-claim) and aggregate (whole-plan) stop-loss. A planned, fully documented cross-border case is exactly the kind of high-cost claim that has to reconcile cleanly against the policy. Our companion guide on how self-funded plans cut costs on complex, high-cost cases covers that math.

How do TPAs, assistance companies, and repatriation fit together?

A cross-border case rarely involves only the TPA. On complex or urgent episodes, an assistance company coordinates the on-the-ground logistics: provider access, guarantees of payment, and, at the end of care, getting the member home. The handoff is what keeps the claim clean. The assistance company or in-country coordinator manages the case and assembles the documentation, then passes a single authorized claim to the TPA for adjudication rather than a stack of foreign paperwork.

When the episode ends in a medically supervised flight home, that is a repatriation. It carries its own MEDIF (the airline’s medical information form clearing the patient as fit to fly) and its own cost file to reconcile. Our guide to medical repatriation in Latin America covers that handoff in detail.

How does MTP work with TPAs?

MTP is the in-country fulfillment layer, not the administrator. It is not a TPA and does not replace one. It works alongside third party administrator companies and assistance desks to deliver the in-country work a TPA is not staffed to do. On a cross-border case, MTP handles:

- Case intake through the TPA’s or assistance company’s desk.

- MEDIF and GOP workflows: fitness-to-fly clearance and payment guarantees managed as routine.

- Vetted, accredited providers matched to the procedure at the facility and accreditation level.

- Claims-ready documentation reconciled to the TPA’s adjudication standard and translated.

- A single case manager across Colombia, Panama, Costa Rica, and Mexico.

Full detail on the engagement model is on our patient logistics partner page.

What should you look for in a cross-border coordination partner?

If you administer or advise a plan with cross-border exposure, the question is usually not which TPA to use, since you already have one. It is who handles the in-country work the TPA is not built to do. That is less a directory or a list of third party administrators for health insurance than a short set of criteria a coordination partner has to meet:

- Local presence in the destination country, not a remote call center.

- A single case manager who owns the file from intake through claim.

- Claims-ready, translated documentation built to a US plan’s adjudication standard.

- GOP and MEDIF fluency: payment guarantees and fitness-to-fly clearance handled as routine, not one-off.

- An accredited provider network vetted at the facility and accreditation level.

- Transparent per-case pricing fixed and known before travel, so there is no open-ended exposure.

A partner that meets all six delivers a foreign episode to the TPA in the same shape as a domestic claim, which is the whole point.

Sources

- Definition and regulatory framing of a third-party administrator: NAIC, Third-Party Administrators (State Licensing Handbook, Ch. 28).

- Share of covered workers in self-funded plans (63% in 2024): KFF, 2024 Employer Health Benefits Survey.

Administering a plan with cross-border cases?

We deliver the in-country coordination and the claims-ready documentation your adjudication needs: case intake, GOP and MEDIF workflows, accredited providers, and a single case manager per file.