Reservar cita

How self-funded plans cut costs on complex, high-cost cases

Por

Por

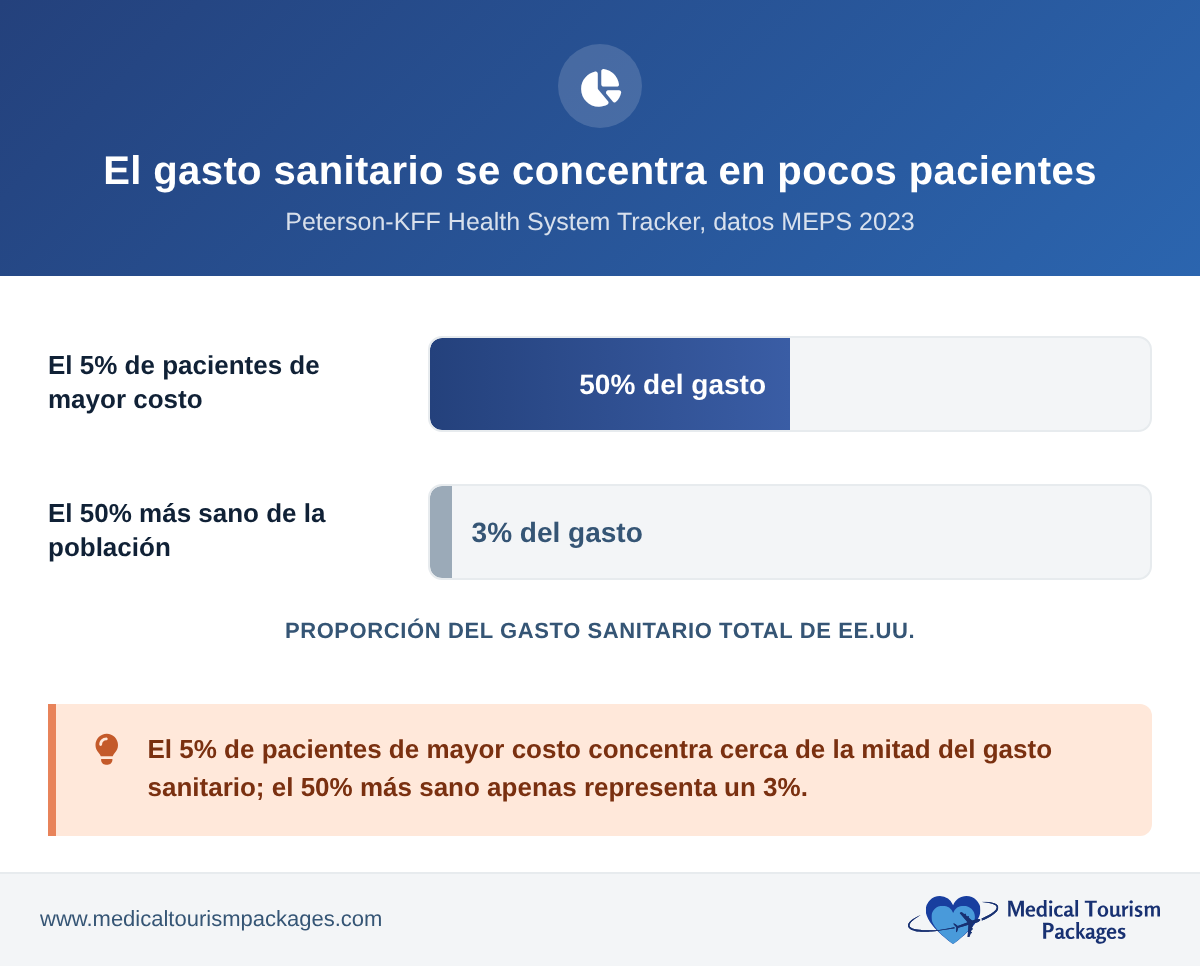

A handful of claimants drive most of a self-funded plan’s spend in any given year. Nationally, the highest-cost 5% of patients account for about half of all health spending, while the entire bottom half of the population makes up only about 3% (Peterson-KFF Health System Tracker, 2023 data). When one of those claimants needs a complex or tertiary procedure, a single bill can move the plan’s entire annual result. That case, not routine utilization, is where the real money sits. It is also where coordinated care abroad produces the largest and cleanest savings.

This guide is a practical look at how to reduce self-funded health plan costs where they actually concentrate: the complex, high-cost claims. It covers what counts as a high-cost claimant, why complex cases are the right lever, how to compare costs honestly against what your plan actually pays, how a cross-border case fits under stop-loss, and how to get members to choose the lower-cost option.

Why do a few high-cost cases drive most of a self-funded health plan’s costs?

In most self-funded plans, a small share of members accounts for a large share of total spend, and that top tier is dominated by complex claims. In stop-loss data, cancer is the single largest high-cost category, followed by cardiovascular disease, with orthopedic and musculoskeletal cases now breaking into the top three. That last category averages about $116,000 per claim (Sun Life 2025 high-cost claims report). Million-dollar stop-loss claims are climbing fast: up 29% in a single year and 61% over four years, per the same analysis.

For a self-funded employer this concentration is not abstract. The plan pays claims directly, so the entire high-cost tail lands on the company’s own books rather than an insurer’s. Stop-loss caps the very largest claims. But the layer beneath the attachment point is absorbed by the plan itself: the six-figure cases that don’t quite trigger reimbursement, or that push up next year’s rates.

That is why most programs deliver so little on the cases that matter. Most cost containment in healthcare targets high-volume, low-cost claims: wellness, network discounts, and utilization management shave a few percent off routine spend. They do almost nothing to the tail. The lever that moves the annual result is the price of the few largest cases.

The high-cost tail usually concentrates in a handful of categories:

- Complex and revision surgery: spinal, joint revision, and multi-stage orthopedic cases.

- Oncology: surgery plus inpatient care, not drug-only regimens.

- Cardiac: valve, bypass, and structural procedures.

- Tertiary, multi-specialty cases: anything needing a high-acuity facility and a long length of stay.

MTP’s employer and plan-sponsor logistics service is built around exactly these planned, high-cost cases.

What do high-cost claimant solutions usually miss?

Most high cost claimant solutions work on the claim after it already exists: repricing, out-of-network negotiation, and case management. These are useful, but they share one limitation: they treat the site of care as fixed.

Changing where a planned complex procedure happens is a larger lever than any post-claim discount. A post-claim negotiation works at the margin of a billed charge. Relocating a planned case to a high-volume accredited center abroad can change the total by a far larger factor, because the price gap between a US-billed complex case and the same accredited care overseas is much wider than any repricer can recover after the fact.

For plan sponsors asking how to reduce healthcare costs for complex, high cost claimants, the site-of-care decision is the one with the most leverage. This is the part of the market MTP serves: planned, non-emergent, complex procedures where there is time to coordinate care in advance.

Which cases are the right candidates?

Not every high-cost claim can move abroad. The model works for planned, non-emergent procedures where there is time to coordinate travel and pre-authorization. Good candidates share a few traits:

- Planned and schedulable: the procedure can wait the weeks needed to arrange travel and authorization.

- Non-emergent: emergencies are handled locally; this is for elective and semi-elective complex care.

- Self-contained: a defined procedure and recovery, rather than open-ended or unpredictable treatment.

- Stable for travel: the patient can fly and tolerate the logistics.

Keeping the program focused on these cases concentrates it where the savings are large and the clinical risk of coordinating abroad is low.

How are the savings actually calculated?

Honest math is what separates a credible cross-border program from vendor spin. Two rules make the comparison defensible.

- Compare against the allowed amount, not list price. The honest comparison is your plan’s net allowed cost at home versus the all-in coordinated cost abroad. Savings quoted off a hospital’s chargemaster or list price are meaningless, and payers know it.

- Count everything on the abroad side. The abroad figure must be all-in: the procedure and accredited facility, the surgeon, accommodation, travel for the patient and a companion, in-country coordination, and aftercare. A procedure-only price set against a fully loaded US allowed amount is not an honest comparison.

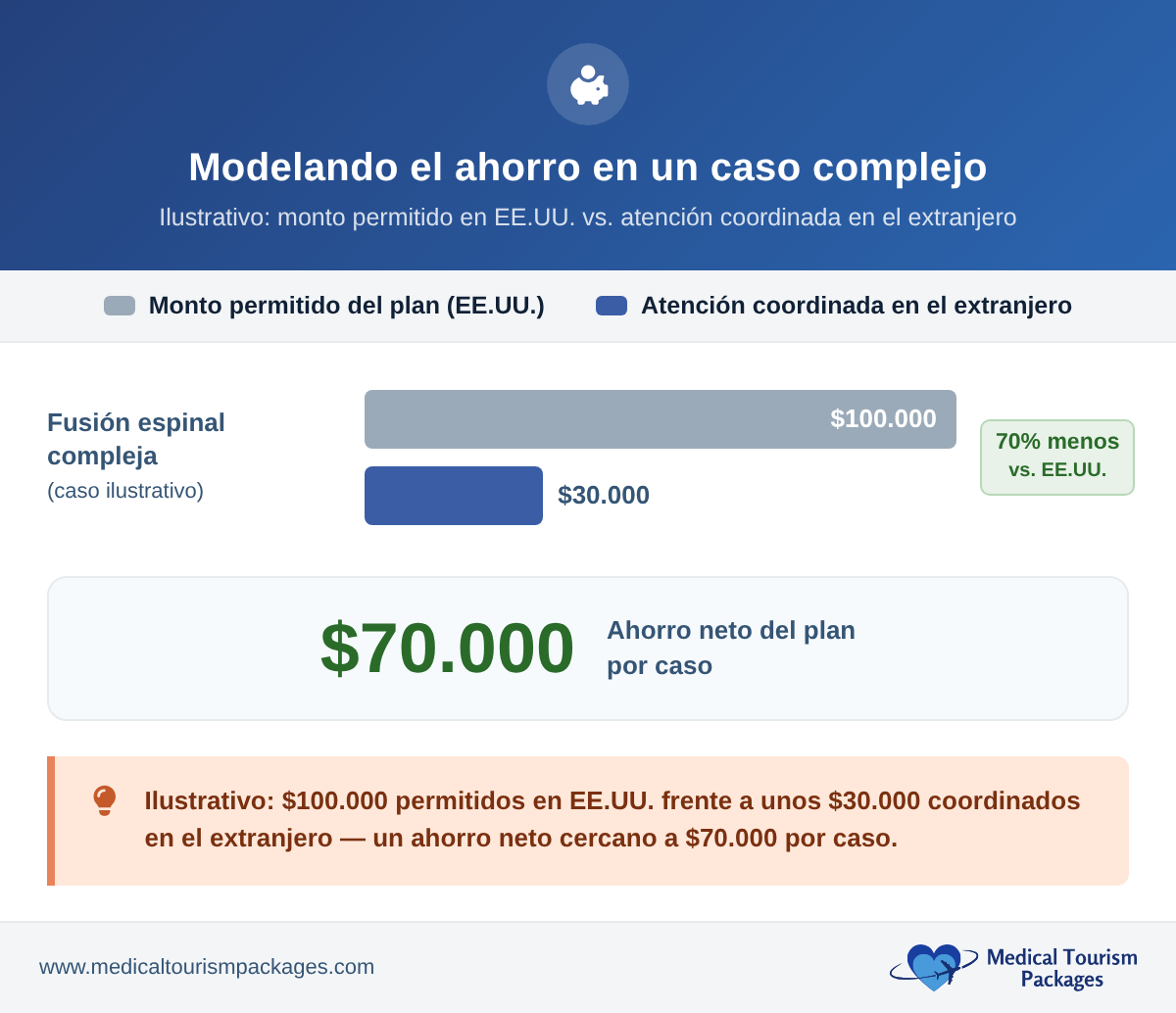

Worked example (illustrative). Take a complex multilevel spinal fusion. In 2023 the mean hospital cost alone for a multilevel fusion was about $55,000, and that excludes surgeon fees, implants, and post-acute care (National Institutes of Health (NIH) lumbar fusion cost analysis, 2023). With those components included, a payer’s allowed amount for a complex case commonly runs to roughly $100,000. A coordinated, all-in case at a Joint Commission International (JCI)-accredited center in Latin America is typically around $30,000. That figure covers the procedure, facility, surgeon, travel for the patient and a companion, lodging, and aftercare. The net plan saving is on the order of $70,000 on a single case. These figures are illustrative: because the honest baseline is your plan’s actual allowed amount, not a published average, MTP models the real numbers for your specific case before any commitment.

The saving is structural, not a discount. It comes from lower facility and labor costs at high-volume accredited centers, bundled fixed pricing, and the absence of the chargemaster markup that inflates US billed amounts. Regional cost and volume data supports the size of the gap; see our Latin America medical tourism cost and growth statistics for the underlying figures.

How does a cross-border case fit with stop-loss?

Self-funded plans carry stop-loss, so a cross-border case has to reconcile cleanly against the policy, or the saving is offset by a coverage dispute.

- Claims-ready documentation: itemized billing and clinical records so the case reconciles against both specific (individual-claim) and aggregate (whole-plan) stop-loss.

- Fixed, known pricing before travel: the all-in price is set in advance, so there is no open-ended exposure and no surprise supplemental billing.

- Coverage confirmed in advance: the case is pre-authorized and reviewed with the plan’s stop-loss carrier before travel, so it is presented as a planned, documented claim rather than a surprise foreign bill.

Bringing the carrier in early matters. A planned, documented, fixed-price case is straightforward for a stop-loss carrier to evaluate; a surprise foreign claim is not. How the third party administrator (TPA) then adjudicates and passes these claims through is its own topic. See our companion guide on TPAs and cross-border claims.

How do you get members to actually use it?

A lower-cost option only saves money if the member chooses it, so the design problem is as much about incentives as logistics. Effective programs align the member’s incentive with the plan’s:

- Waived or reduced cost-share: the member pays little or nothing out of pocket for the cross-border option.

- Paid travel and lodging: the plan covers travel for the patient and a companion, so choosing the cheaper option costs the member nothing extra.

- Shared-savings payment: the member receives a cash benefit funded from the plan’s saving.

The logic is simple: make the lower-cost, high-quality option also the best financial outcome for the employee, and utilization follows.

Does this work for small and mid-sized employers?

Yes, and the case is arguably stronger for smaller plans. A single six-figure claim hits a small or mid-sized business (SMB) self-funded plan far harder than it hits a large one, because there are fewer members to absorb it. Effective healthcare cost containment for SMBs therefore depends more on protecting against the individual large case than on squeezing routine spend.

Because coordinated cross-border care is priced per case, there is no standing program cost and no minimum enrollment. A mid-sized employer can use it for a single planned procedure and still protect the year. One well-managed case can be the difference between an on-budget plan year and a bad one.

What does MTP do in the chain?

MTP’s role is narrow and operational: it is the in-country logistics layer, not the plan, the network, or the carrier. For a plan sponsor or TPA, MTP handles:

- Provider matching at accredited centers appropriate to the procedure.

- Full travel and recovery coordination for the patient and a companion.

- A single case manager per file, so there is one point of contact from referral through aftercare.

- Claims-ready documentation for the plan and its stop-loss carrier.

MTP coordinates cases across Colombia, Panama, Costa Rica, and Mexico. Full detail on the employer and plan-sponsor engagement model is on our patient logistics partner page.

Sources

- Concentration of health spending (top 5% ≈ half of all spending): Peterson-KFF Health System Tracker, 2023 Medical Expenditure Panel Survey (MEPS) data.

- High-cost claim conditions and rising million-dollar stop-loss claims: Sun Life High-Cost Claims report, 2025.

- U.S. lumbar fusion cost (multilevel hospital cost, 2023): Cost and utilization trends of lumbar fusion, NIH/PMC.

Have a high-cost case coming up?

Send us the procedure and your plan’s allowed amount, and we will model the all-in coordinated cost and the net saving. No program commitment required.